Subtotal ₹0.00

Email :50

Despite global uncertainties private capital inflows have more than doubled in Q1 2026 (YoY), driven largely by domestic capital, with NCR and Pune garnering most of the capital.

According to a latest report of Knight Frank India, private equity investment in Indian real estate recorded USD 637 million across 9 transactions in Q1 2026, marking a 2.1x increase over Q1 2025 (USD 300 million across 3 deals). While the increase reflects improved transaction activity, investment momentum remains selective and is largely being driven by domestic capital, against a backdrop of continued global uncertainty.

Source: Knight Frank Research, Venture Intelligence

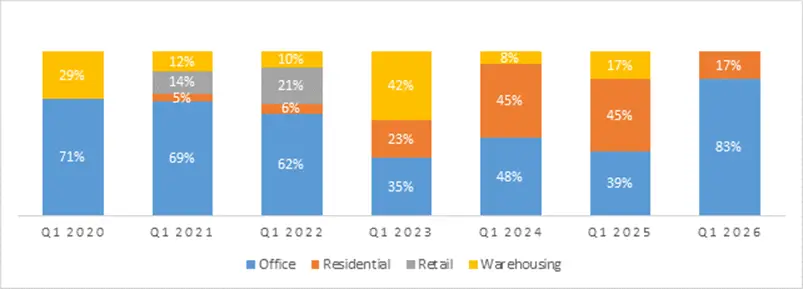

Office remains the preferred asset class for investment

Office assets led investment activity with USD 529 mn, accounting for 83% of total inflows across four transactions. All deals involved stabilised, income-generating assets, indicating a clear investor preference for yield visibility and asset-level security over development exposure. Three of the four transactions were structured as equity, suggesting improving conviction on pricing for leased office assets.

Residential capital continues to favour structured credit

Residential investments stood at USD 108 million across five transactions, contributing 17% of total activity. The quarter remained firmly debt-led, with four out of five deals structured as debt. Capital deployment was directed toward mid-income and luxury projects across various stages, reflecting a continued preference for downside protection in a segment where exit timelines remain less predictable.

Warehousing and retail record no transactions in Q1 2026

Warehousing and retail segments recorded no transactions in Q1 2026, a notable contrast to their combined USD 885 million contribution in 2025. In warehousing, the absence of activity reflects a more conservative underwriting stance amid elevated financing costs, and limited availability of stabilised, institutionally owned assets at acceptable entry yields.

Retail’s inactivity is consistent with its historically episodic investment pattern. Capital deployment in this segment has been confined to select large-format, high-quality assets, and no such opportunity closed in the quarter. Both segments are expected to see renewed activity as the year progresses, with investor interest in income-producing assets remaining intact.

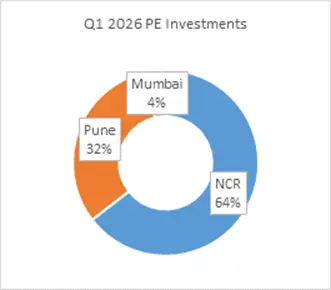

Capital deployment concentrated in select markets

Source: Knight Frank Research, Venture Intelligence

Investment activity remained highly concentrated, with NCR accounting for USD 411 million (65%) and Pune USD 203 million (32%) of total inflows. Mumbai saw limited activity at USD 23 million, while a Bengaluru deal between a Japanese investor and an Indian listed real estate player was concluded at an undisclosed value.

This concentration underscores a risk-calibrated deployment approach, with capital favouring markets that offer stronger leasing depth, institutional-grade assets, and clearer exit visibility.

NCR and Pune Dominate Q1 2026 Investment Activity

Source: Knight Frank Research, Venture Intelligence

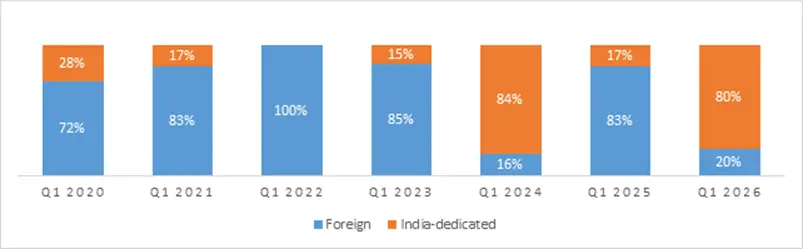

Domestic capital anchors activity amid global caution

Indian funds invested USD 510 million, accounting for 80% of total investments and effectively anchoring Q1 activity. This reflects both the availability of domestic dry powder and a more measured approach by foreign investors.

Foreign capital, at USD 128 million (20%), remains selective, with deployment largely restricted to stabilised assets. Currency hedging costs, valuation gaps, and continued caution toward development risk continue to influence cross-border investment decisions.As a result, current investment momentum is being shaped more by domestic liquidity than by a broad-based return of global capital.

Domestic Capital Drives Investment Activity Amid Global Caution

Source: Knight Frank Research, Venture Intelligence

According to Shishir Baijal, International Partner, Chairman and Managing Director, Knight Frank India, the doubling of PE investment volumes relative to Q1 2025, combined with a decisive tilt toward ready office assets and structured residential credit, suggests that investors are increasingly comfortable with the risk-return profile in select segments. Office remains the anchor of institutional confidence, and domestic capital’s leadership reflects both the maturation of Indian alternative asset management and the relative friction still facing cross-border capital. The broader recovery in 2026, which we expect to build through the year, will depend on how quickly valuation alignment improves in the development pipeline and whether the macro environment remains supportive.